In-Depth Review of Economic Events and Corporate Reports for January 13, 2026: US CPI, Bank of England Governor's Speech, Housing Sales and US Budget Statistics, API Oil Data, and Financial Results from Companies in the US, Europe, Asia, and Russia

Tuesday presents a busy agenda for global markets: investors are focused on the December inflation data from the US, which is capable of setting the tone for the dynamics of risk assets. In Europe, attention is directed toward the speech by the Governor of the Bank of England, which may impact the value of the pound and sentiment in the UK market. Simultaneously, in the US, the fourth quarter earnings season kicks off: major banks and companies will report results, providing the first gauges on the state of the business economy. The energy sector is monitoring the evening oil inventory statistics (API), complementing the picture after the macro data release. It is critical for investors to evaluate indicators in conjunction: US inflation ↔ Fed expectations ↔ bond yields ↔ currencies ↔ commodities ↔ risk appetite.

Macroeconomic Calendar (Moscow Time)

- 12:00 PM – United Kingdom: Speech by Bank of England Governor Andrew Bailey at an economic forum.

- 4:30 PM – US: Consumer Price Index (CPI) for December.

- 6:00 PM – US: New home sales (New Home Sales, October data).

- 10:00 PM – US: Federal budget for December (monthly Treasury report).

- 12:30 AM (Wednesday) – US: Weekly oil inventories according to API data.

Key Points to Watch in US CPI

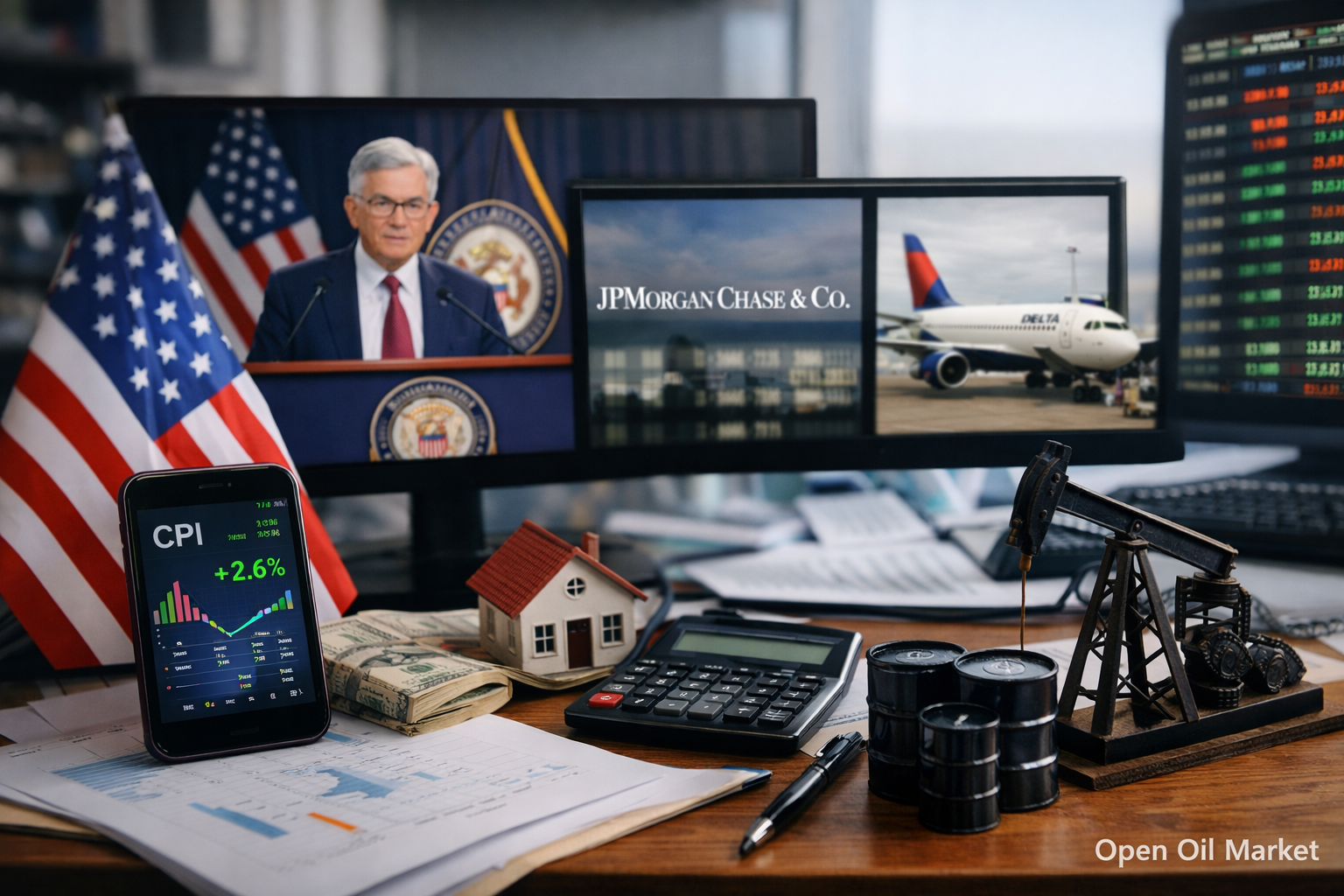

- Core Inflation (Core CPI): This is a key indicator for future Fed policy. Predictions indicate a slowdown in the core index to approximately 2.6% year-over-year; confirmation of a declining trend would bolster expectations for easing monetary policy and support the stock market. Conversely, if Core CPI exceeds forecasts, it may amplify hawkish sentiments at the Fed, elevate Treasury yields, and exert pressure on stocks, especially in the tech sector.

- Price Composition: Investors will analyze the contribution of services (especially housing) and goods prices to the overall index. A slowdown in rental and service price growth signals diminishing inflationary pressure in resilient components. Conversely, an unexpected rise in these categories could indicate lingering inflation inertia.

- Market Reaction: Sharp movements in the US dollar and bond yields may occur immediately after the CPI release. A stronger dollar alongside high CPI figures could reduce commodity prices (oil, gold) and currencies from emerging markets, while softer inflation data would weaken the USD and create a favorable environment for risk assets.

United Kingdom: Speech by the Bank of England Governor

- Tone of Monetary Policy Commentary: Andrew Bailey’s speech at 12:00 PM Moscow Time will be a significant event for the pound and the UK market. If the Bank of England Governor suggests that inflation in Britain remains elevated and further tightening may be required, this may support the GBP and the banking sector, but could exert pressure on the FTSE 100. Softer, 'dovish' signals (e.g., confidence in falling inflation and a pause on rate hikes) would likely weaken the pound, which, however, would be positively perceived by exporters and British export-oriented company stocks.

- Assessment of the UK Economy: Investors will also look for hints regarding the state of the UK economy on the brink of 2026 in Bailey's speech. Comments on growth rates, labor market conditions, and credit availability may adjust expectations around Bank of England policy. Any mentions of financial stability or the banking sector will be vital for understanding risks and the sentiments of the regulator.

US: Housing Market and Budget Indicators

- New Home Sales: Data on New Home Sales (for October) will provide additional insight into the state of the housing market in the US. Although this indicator is lagging, trends in new home sales reflect the impact of high-interest rates on buyer demand. An improvement or stability in this indicator may signal resilience in consumer demand and support shares of homebuilders, while a sharp decline would indicate a cooling in the real estate market due to costly mortgages.

- US Federal Budget: The evening Treasury report on the December budget will reveal the size of the deficit or surplus at year's end. A significant deficit will remind the market of fiscal risks, including rising public debt and potential increases in borrowing in the new year. While monthly budget data rarely impacts the market immediately, its analysis is essential for long-term investors: a tendency toward increasing deficits may eventually pressure bond yields and needs consideration in strategies for 2026.

Earnings Reports: Before Market Open (BMO)

- JPMorgan Chase (JPM): The largest bank in the US will announce its results before the session begins. Investors hope to see how high-interest rates have impacted net interest income and the bank's margin. Key focuses include lending volumes and reserves for potential loan losses: an increase in reserves may signal management’s caution regarding economic prospects. Also important are the trading and investment banking results for JPMorgan in the fourth quarter: strong performance would indicate Wall Street's resilience, while weak investment banking results would confirm a continued downturn in the M&A and IPO markets. JPMorgan's management outlook for the US economy and banking sector in 2026 will be a crucial benchmark for the financial market.

- Bank of New York Mellon (BK): One of the leading global custodian banks will present its results before market open. For BNY Mellon, commission income from custody and asset management services, which depend on market dynamics and institutional client activity, is crucial. Investors will assess whether the volume of assets under management/storage increased amidst year-end market volatility. Another focus is on interest income from client deposits: rising rates may have improved margins but could also stimulate fund outflows to higher-yielding instruments. Management's insights on the state of global markets and capital inflows/outflows will provide direction for financial sector stocks in Europe and the US.

- Delta Air Lines (DAL): One of the world's largest airlines will report for the fourth quarter, including the holiday season. Investors will look for signs of consumer demand resilience in air travel: high load factors and passenger traffic figures will indicate that travel remains a priority for consumers despite the economic situation. Particularly important are unit revenue metrics (PRASM) and commentary on airfares – this will reflect the airline's ability to pass on increased costs (fuel, personnel) to customers. If Delta improves its margins or provides an optimistic revenue outlook for 2026, this will bolster the entire airline sector. However, a cautious tone regarding business travel or costs may act as a restraining factor for the sector's stocks.

- Concentrix (CNXC): The American business process outsourcing provider will report before trading begins. The company is known for providing contact center and client support services to corporations worldwide. Investors are interested in Concentrix's revenue growth amid digitalization and its merger with Webhelp (closed earlier in 2025) – the synergy from this combination could have scaled up the business. Profitability metrics will also be analyzed: whether the operating margin was maintained amidst integration costs and inflation in service salaries. Concentrix's outlook for demand from corporate clients in 2026 will signal whether companies continue to invest in customer service and IT outsourcing even amid economic uncertainty.

Earnings Reports: After Market Close (AMC)

- Significant releases after the main session closes on Tuesday are not expected. The corporate calendar for the evening of January 13 is sparse – most major issuers from the S&P 500 and Nasdaq indices have scheduled their financial results for the following days of the week. Thus, investors will not see significant corporate intrigue after the market closes, and the news backdrop in the evening will be relatively calm.

Other Regions and Indices: S&P 500, Euro Stoxx 50, Nikkei 225, MOEX

- S&P 500 (US): On Tuesday, the American stock market enters a new earnings season. Morning reports from heavyweight companies like JPMorgan and Delta will set the tone for financial and transportation sectors. Since the S&P 500 previously reached high levels, investors are carefully evaluating the first reports: can corporate profits meet the confident market expectations? Additionally, the dynamics of the S&P 500 on this day will depend on the CPI data – strong bank earnings may shift the focus from macroeconomics to micro-level, but unexpected inflation figures may induce overall market fluctuations.

- Euro Stoxx 50 (Europe): No quarterly earnings publications are scheduled among the blue chips in the Eurozone on January 13. European markets will primarily focus on external factors – market reactions to US inflation data and signals from the UK. The absence of major corporate drivers in the Euro index means that macroeconomic news and currency dynamics (especially EUR/USD and GBP/USD after Bailey's speech) could play a decisive role. It is also worth mentioning some local reports; for example, the UK company Games Workshop (FTSE 250) will publish half-year results, and in Germany, agricultural holding Südzucker will report quarterly – these releases are important within their sectors but are unlikely to affect the broader market.

- Nikkei 225 (Japan): The Japanese market continues to publish results from companies with non-standard fiscal years. There are no significant reports from Nikkei 225 giants on Tuesday; however, investors are monitoring corporate news from smaller firms. Notably, one prominent company, the pharmacy supermarket chain Cosmos Pharmaceutical, will present financial results for the first half of the fiscal year, reflecting consumer activity in the pharma retail sector. Overall, trading activity in Tokyo will be more influenced by the overall sentiment in global markets following the US data release; the Japanese index is sensitive to changes in risk appetite and yen fluctuations, so any surprises in the CPI may also impact the Nikkei 225 dynamics.

- MOEX (Russia): No significant financial reporting from major issuers is expected on the Moscow Exchange on January 13 – the quarter and annual results season for Russian companies traditionally starts later in January and February. Some activity may be observed related to operating updates from specific firms or boards of directors regarding dividends, but these events will not significantly impact the MOEX index. In the absence of domestic drivers, the Russian market will follow global market sentiments and oil price dynamics: US CPI data and external factors will mainly determine the direction for the ruble and the cost of Russian assets on Tuesday.

End of Day: What Investors Should Pay Attention To

- US CPI: The release of inflation data in the United States is the primary trigger for the day. Investors should prepare for a surge in volatility at 4:30 PM Moscow Time: deviations of actual CPI from forecasts will instantly reflect in the dollar's exchange rate, bond yields, and global stock indices. Special attention should be given to core inflation; its slowdown may give momentum to stock prices, while unexpectedly high figures may spark discussions around the Fed's next steps and potentially lead to a short-term risk sell-off.

- Speech by the Bank of England Governor: Andrew Bailey's daytime speech may shift expectations around UK rates. Investors engaged in the currency markets should closely monitor the GBP's reaction: any hawkish comments from Bailey could strengthen the pound and influence European financial stocks, whereas a softer tone might have the opposite effect. This speech will also provide insights into regulators' sentiments in Europe as the year begins.

- Corporate Reports in the US: The start of the earnings season sets thematic movements within the market. Strong results and forecasts from JPMorgan, Delta, and other companies before the market opens may support their respective sectors (financial, transportation), shifting the focus from macro statistics to corporate narratives. However, investors should compare corporate trends with macroeconomic sentiment: for instance, even strong bank reports may be overshadowed by negativity from high CPI figures, and conversely, moderate inflation may amplify the positive effect of strong corporate profits.

- Oil and Commodity Prices: The oil market will receive signals from the API's crude oil inventory report (12:30 AM Wednesday). Although this indicator is preliminary, an unexpected increase or decrease in inventories could induce price movements in oil, reflecting on the stocks of the oil and gas sector and currencies of commodity countries. In conjunction with inflation data (especially energy components of CPI), this will help to understand the trajectory of the commodity segment. Commodity investors should remain vigilant after major trading closes.

- Risk Management in a Busy Day: A combination of significant macro data and the first major reports creates conditions for heightened volatility. It is advisable to predefine acceptable fluctuation ranges for the portfolio and set stop orders or hedging positions, especially when trading over the short term. In such an information-rich market, it is sensible to avoid excessive leverage and emotional decisions: it is better to wait for the release of key indicators and then make informed investment steps based on facts rather than forecasts.