Analysis of Key Economic Events and Corporate Reports for Saturday, November 1, 2025: APEC Summit in South Korea, Corporate Earnings Releases from S&P 500, Euro Stoxx 50, Nikkei 225, and MOEX. Recommendations for Investors.

Saturday, November 1, sets an intriguing backdrop for investors: the APEC Summit in South Korea is taking place on its second day, where leaders are discussing key trade and development issues in the region, while markets are preparing for a series of quarterly reports from major companies. The focus will be on the economic agenda in Asia and the U.S., as well as the corporate earnings reports from the U.S., Europe, Asia, and Russia. Investors should closely monitor the outcomes of the negotiations at the APEC summit and the corporate earnings releases that will follow over the weekend, which will shape risk perception and expectations regarding interest rates.

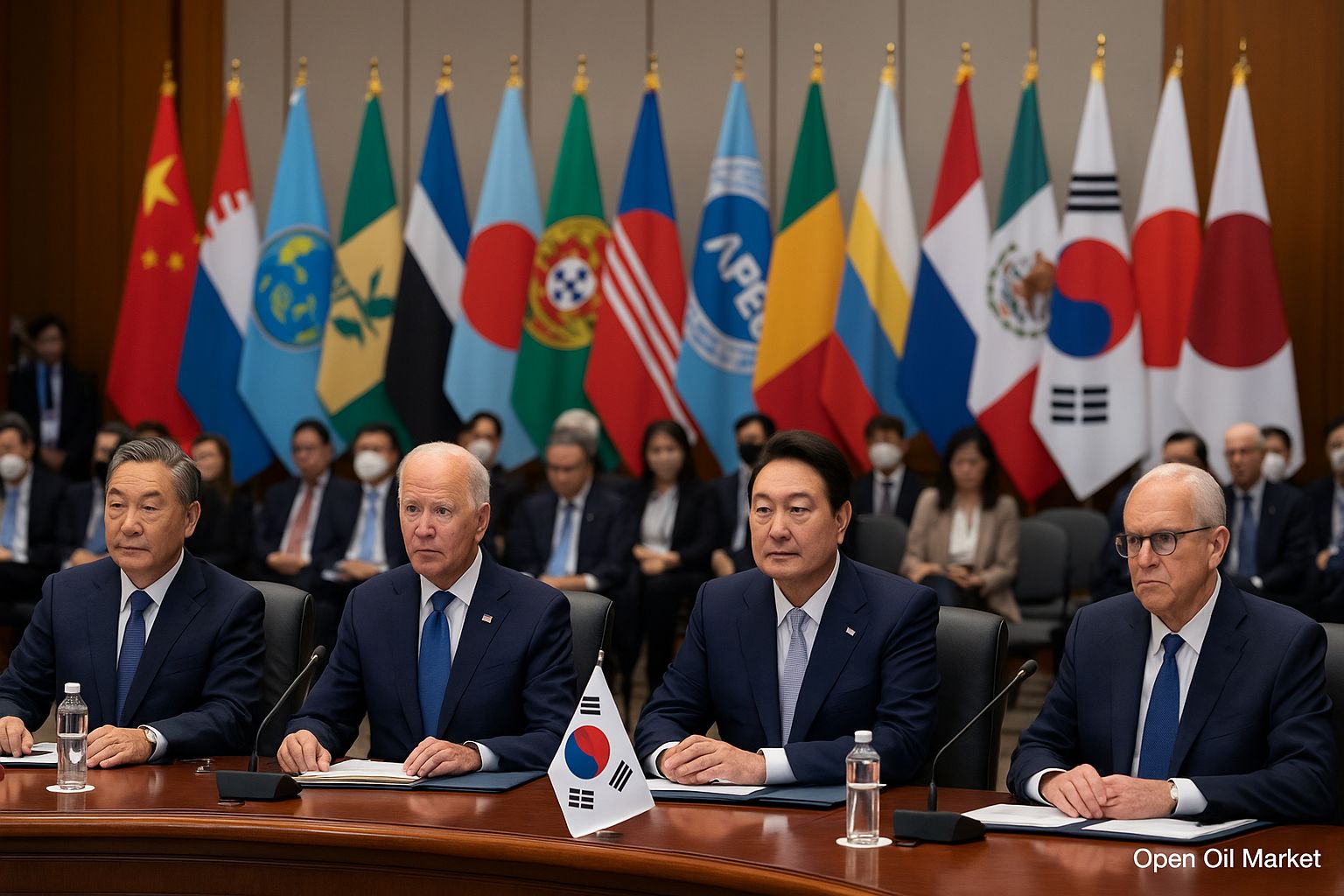

APEC Summit 2025 — Day 2

On the second day of the APEC (Asia-Pacific Economic Cooperation) summit in South Korea, the discussions remain centered on trade and economic cooperation, investment, and energy security. Leaders are addressing:

- dismantling trade barriers: advancing U.S.-China negotiations on the summit's sidelines, promoting bilateral agreements on logistics and key resources;

- climate and sustainable development: agreeing on new commitments to reduce carbon footprints and support the region’s green economy;

- innovation technologies: initiatives on digitalization and cybersecurity, including the expansion of projects in AI and fintech;

- APEC expansion: discussions on the integration of new members (e.g., East Timor) and strengthening regional security through joint economic projects.

Against this backdrop, Asian markets are cautiously responding to signals of extending economic activity, as well as external political news. Any signs of successful trade negotiations could support risk appetite and the rise of Asian indices, while increased tensions may lead to a flight to safe assets (yen, gold).

Macroeconomic Background

It is a holiday in the Russian market: November 4 marks National Unity Day, making Monday the next trading day. The Central Bank of Russia has set the official dollar exchange rate on Saturday, November 1, at approximately 80.98 rubles, slightly higher than the previous day's rate. The oil market is demonstrating moderate price declines: Brent is trading around $64–65/barrel, losing ground due to a strong dollar and overproduction. Investor focus at the beginning of the week will shift to global PMI publications and other statistics: revisions of the manufacturing PMI indices for the U.S., Eurozone, and China are expected ahead of the weekend, which will set the tone for central bank interest rate expectations. The state of global inflation and consumer price dynamics in major economies remain key drivers for currency and bond valuations.

Corporate Reports from the U.S. and Asia

- Grab (NASDAQ: GRAB, Singapore/U.S.): Earnings results for Q3 2025 are expected to be released after market closure on November 3, followed by a management conference call.

- Goodyear (NYSE: GT, U.S.): Will publish its Q3 report after market closure on November 3; presentation and comments will take place the following day.

- Ichor Holdings (NASDAQ: ICHR, U.S.): Will release financial results for Q3 immediately after market closure on November 3, followed by a call for investors.

- Advanced Micro Devices (NASDAQ: AMD, U.S.): Will release its Q3 report after market closure on November 4; investors are watching for semiconductor business data.

- Amgen (NASDAQ: AMGN, U.S.): Will release Q3 results after market closure on November 4; market attention is on new drug sales results.

- Chinese and Asian issuers: While major Asian markets are closed on Saturday, attention remains on recent events in the region – for instance, IPOs and reports from major Chinese companies (tech giants, banks), which will be released shortly after holidays in mainland China.

Corporate Reports from Europe

- Ryanair (Dublin/Frankfurt): Report for September 2025 will be released before market opening on November 3; focus on passenger traffic and fuel futures prices.

- Associated British Foods (LSE: ABF, U.K.): Will publish its report before trading starts on November 4; analysts forecast moderate revenue growth due to a diversified portfolio (food, retail).

- BP (LSE: BP, U.K.): Will report before trading starts on November 4; investors are awaiting comments on oil extraction and gas projects amid price volatility.

- Ferrari (NYSE/MTA: RACE, Italy/U.S.): Q3 report will be released after market closure on November 4; focus on sales of luxury cars and development of new models.

- Pfizer (NYSE: PFE, U.S.): Will report after market closure on November 4; the market is awaiting updates on vaccine sales and medications in Q3.

- Uber (NYSE: UBER, U.S.): Reporting after market closure on November 4 – investors are interested in delivery and taxi service dynamics.

- Toyota Motor (TSE: 7203, Japan): Will release its financial report on November 5 before market opening – key metrics include revenue from vehicle sales and electrification costs.

- McDonald’s (NYSE: MCD, U.S.): Will present results on November 5 before trading begins; market attention will be on margins and sales of coffee and burgers.

- Pandora (OMX: PNDORA, Denmark): Will report after market closure on November 5; investors are monitoring jewelry demand and consumer behavior.

Corporate Reports from Russia and the CIS

- MOEX Group (MOEX): Disclosure of trading volumes for October 2025 is scheduled for November 1. This data will indicate investor activity on the Moscow Exchange following the October reports from major banks and commodity companies.

- Major banks and corporations in Russia: Sberbank (usually publishes a summary for the first nine months), Gazprom Neft, Norilsk Nickel, Rosneft, among others – presented their results for the first nine months at the end of October. Investors will compare these results with expectations regarding central bank interest rates and the dynamics of the ruble.

- Dividends and Corporate Decisions: On November 1, the deadline for dividend payments by some Russian issuers (for example, EuroTrans, MD Medical) will expire. Attention should be paid to corporate news in the following week in anticipation of the IFRS reporting season in Russia.

What Investors Should Focus On

It is important for investors to correlate geopolitical factors with corporate dynamics. First and foremost, keep an eye on the outcomes of the APEC summit: progress in trade negotiations between the U.S. and China or new climate initiatives could change global sentiments. Secondly, key reports from major companies within the S&P 500, Euro Stoxx 50, Nikkei 225, and MOEX will set the tone for market forecasts for Q4. Also, assess the market's reaction to energy trends: sharp fluctuations in oil prices or changes in OPEC+ policy impact stocks and currencies of emerging markets. Among macroeconomic indicators, global PMIs and industry statistics will be in focus early in the week – strong figures could fuel expectations for a tightening of monetary policy. Conservative investors might hedge risks through currency assets and gold, while risk-takers should consider diversifying their portfolios in light of potential volatility following a news-heavy week.