Key News from the Oil, Gas, and Energy Sector for Wednesday, May 27, 2026: Oil at Key Levels, Tension in the LNG Market, Coal Demand, Electricity, Renewables, Fuels, and Risks for the Global Energy Sector

Wednesday, May 27, 2026, marks a significant day for the global fuel and energy sector. The world oil market remains influenced by geopolitical risks surrounding the Middle East, supply disruptions through key maritime routes, and expectations for new inventory data from the U.S. For investors, sector participants, fuel companies, oil firms, refineries, and traders, the primary concern is not just the current price of Brent and WTI, but also the resilience of the entire supply chain—from oil and gas production to refining, logistics, electricity, coal, and renewables.

The market enters a new trading session with heightened sensitivity to news. Oil is trading near the psychologically significant zone of $100 per barrel, the gas market is facing shortages of specific LNG supplies, European electricity markets are preemptively pricing in premiums for winter risks, and coal is once again becoming a strategic resource for Asia. Against this backdrop, renewables and energy storage are solidifying their strategic role but fail to alleviate short-term tensions in the energy balance.

Oil: Brent at a Key Mark and Risk on the Horizon for the Middle East

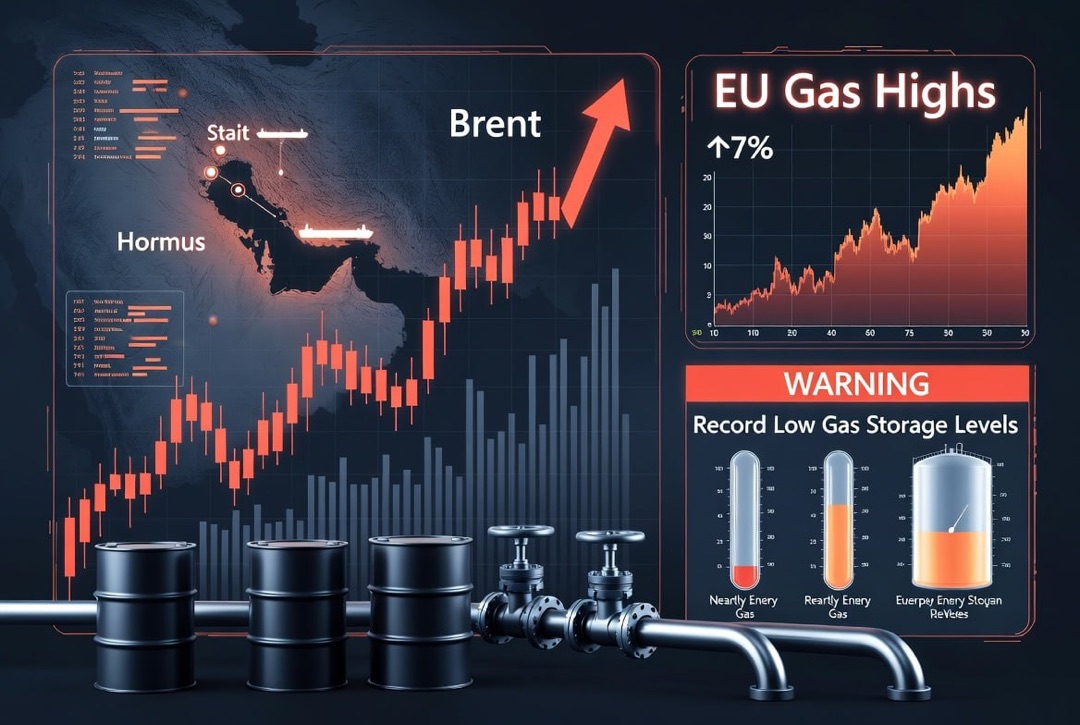

The main topic for the oil market on May 27 is the maintenance of elevated geopolitical premiums. Brent remains close to the $100 per barrel zone after sharp fluctuations related to new military and diplomatic signals surrounding Iran and the Persian Gulf. For the global oil market, this means that traders are reassessing not only the balance of supply and demand but also the risk of disruptions in transportation.

The most sensitive factor remains the Strait of Hormuz. A significant portion of the world’s maritime oil and oil product exports traditionally passes through this route. Even if physical deliveries do not completely halt, insurance premiums, freight rates, logistics, and the risk of delays directly impact oil prices, refinery margins, and fuel costs for end consumers.

- For investors in the oil and gas sector, a key indicator is the stability of Brent above $95–100.

- For oil companies, logistics, export routes, and tanker fleet availability are crucial.

- For refineries, the main factor becomes the differential between crude prices and the cost of gasoline, diesel, and jet fuel.

OPEC+: The Market Awaits June Production Decision

The second significant factor is expectations regarding OPEC+ policy. The market is discussing a scenario of moderate increases in production targets for July. For the oil market, this creates a complex configuration: on one hand, additional barrels could partially alleviate supply shortages; on the other hand, the actual capacity of various producers to rapidly increase exports is limited by geopolitics, logistics, and internal production factors.

For investors, this means that the headline figures on quotas are no longer the sole benchmark. It is much more important to observe actual production, export flows, availability of spare capacity, and the state of port infrastructure. If the market sees an increase in quotas without a comparable rise in physical deliveries, the premium in oil prices may persist.

U.S.: Oil and Product Inventories Become Key Demand Indicator

On Wednesday, the market will closely monitor the weekly U.S. statistics on oil and product inventories. Recent data has shown a notable reduction in commercial oil and gasoline stocks against a backdrop of stable demand and high exports. This is particularly important for the global market ahead of the summer driving season, when gasoline and jet fuel consumption traditionally increases.

The reduction in U.S. oil inventories heightens tensions in the market as U.S. supplies become increasingly vital for buyers in Europe and Asia. If new data indicates a further decline in crude, gasoline, or distillate stocks, this could support Brent, WTI, and petroleum product quotes. For refineries, this presents both an opportunity and a risk: high margins sustain profitability, but expensive oil and logistical constraints raise operational costs.

Gas and LNG: Europe and Asia Compete for Flexible Supplies

The gas market remains one of the most strained segments of the global energy sector. The key risk is associated with LNG supplies from the Middle East and cargo redistribution between Europe and Asia. The extension of force majeure restrictions on Qatari LNG supplies to Europe intensifies competition for American, African, and Australian LNG.

For Europe, the situation is particularly sensitive due to the need for preemptive preparations for the winter season. Low gas storage levels and high spot prices for LNG cargoes place pressure on the electricity sector, industry, and the municipal sector. Asia, on the other hand, faces increasing energy demand due to heat, industrial activity, and the need to maintain stability in energy systems.

- European buyers are striving to replace missing LNG cargoes with alternative supplies.

- Asian importers are ramping up purchases of gas and coal to cope with peak summer demand.

- American LNG exporters enjoy a price advantage, but the U.S. domestic market remains heterogenous.

Electricity: Winter Premium in Europe and Increased Pressure on Networks

The European electricity market is preemptively pricing in a premium for winter risks. Prices are influenced by several factors: gas costs, limited hydro generation, storage conditions, LNG imports, and the resilience of network infrastructure. Germany and Italy, where gas plays a significant role in the energy balance, remain particularly sensitive to rising fuel costs.

For investors in the power sector, this means a growing valuation for companies involved in flexible generation, networks, energy storage, and peak load management. The energy crisis increasingly shifts from a "fuel deficit" format to a "flexibility deficit" format: the market demands not only megawatts of installed capacity but also the ability to quickly balance supply and demand.

Coal: Asia Returns Coal to the Center of Energy Security

The coal market is receiving support once again due to heat, rising electricity consumption, and domestic production issues in certain countries. In India, peak loads on the energy system have hit record levels, prompting coal companies to accelerate deliveries to power plants. In China, additional safety inspections following accidents at mines limit some production, creating risks for the supply of coking and thermal coal.

This is an important signal for the global energy sector: despite the long-term energy transition, coal remains a backup tool for energy security. As gas prices rise, LNG becomes less accessible, and electricity demand increases, Asian countries are ramping up coal consumption to stabilize energy systems.

- India is boosting coal supplies amid heat and high electricity demand.

- Chinese production restrictions may support coal prices in Asia.

- Japan and South Korea may increasingly utilize coal in the context of expensive LNG.

Refined Products and Refineries: Gasoline, Diesel, and Jet Fuel Remain in Focus

The refined products market remains robust due to seasonal demand, logistical disruptions, and limited availability of specific grades of crude. For refineries, the key factor becomes the refining margin. High prices for diesel, gasoline, and jet fuel can sustain profitability for refiners, especially in the U.S. and in markets with access to stable crude supplies and export infrastructure.

However, fuel companies continue to face risks. High oil prices increase working capital, and freight and insurance volatility complicates supply planning. In an unstable market, companies that have diversified procurement channels, flexible logistics, access to storage, and the ability to quickly switch production structures between gasoline, diesel, fuel oil, jet fuel, and petrochemical feedstock will thrive.

Renewables and Storage: Long-Term Trend Gains Momentum, but Short-Term Deficits Persist

In the face of high oil and gas prices, the renewables sector gains an additional strategic argument. Solar and wind energy, along with storage systems, are becoming increasingly important components of the global energy balance. In April, wind and solar together produced more electricity than gas generation worldwide for the first time, underscoring the acceleration of the energy transition.

However, it is important for investors to not confuse the long-term trend with short-term stability of energy systems. Renewables reduce dependence on imported fuels but require investments in infrastructure, storage, backup generation, and digital demand management. Therefore, the most appealing opportunities are not only for solar and wind producers but also for companies operating in battery, network infrastructure, balancing systems, and industrial energy efficiency segments.

What is Important for Investors and Energy Sector Companies on May 27, 2026

Wednesday will be a day of heightened focus on market signals. Investors, oil companies, fuel traders, refineries, and electricity market participants should monitor not just one indicator, but the entire range of factors affecting the global energy sector.

- The dynamics of Brent and WTI near key price levels.

- New data on oil, gasoline, and distillate inventories in the U.S.

- News on LNG supplies, particularly from Qatar, the U.S., and Australia.

- European gas and electricity prices ahead of the winter season.

- The state of the coal market in India, China, Japan, and South Korea.

- The refinery margin and demand for gasoline, diesel, and jet fuel.

- Investments in renewables, energy storage, and grid infrastructure.

The main takeaway for the market is that the global energy sector is entering a phase where fuel prices are increasingly influenced by geopolitics, logistics, and infrastructure accessibility. Oil, gas, electricity, renewables, coal, refined products, and refineries can no longer be analyzed in isolation. For global investors, the key strategy remains the search for companies with sustainable cash flow, control over logistics, access to raw materials, and the ability to profit from both traditional energy and the energy transition.