The Global Fuel and Energy Sector Enters Thursday, May 28, 2026, with a Rare Combination of Factors: Oil Prices Retreat on Expectations of De-escalation Around the Strait of Hormuz, While Gas, LNG, Electricity, Coal, Oil Products, and Refineries Continue to Operate in Conditions of Heightened Volatility

For investors, market participants in the energy sector, fuel companies, oil firms, and power operators, the key question of the day goes beyond the current price of Brent or WTI. Much more critical is how resilient the recovery in logistics will be, how quickly oil and gas flows normalize, whether refineries can maintain their margins, and if the power sector can withstand rising demand fueled by heat, data centers, and the structural energy transition.

The global energy market remains exceedingly sensitive to news from the Middle East, OPEC+ decisions, U.S. inventory dynamics, and demand from China and India, as well as the competition between Europe and Asia for LNG supplies. It is not individual quotes that take the forefront but rather the ability of energy supply chains to adapt to a prolonged period of geopolitical instability.

Oil: Brent Retreats, But Risk Premium Remains

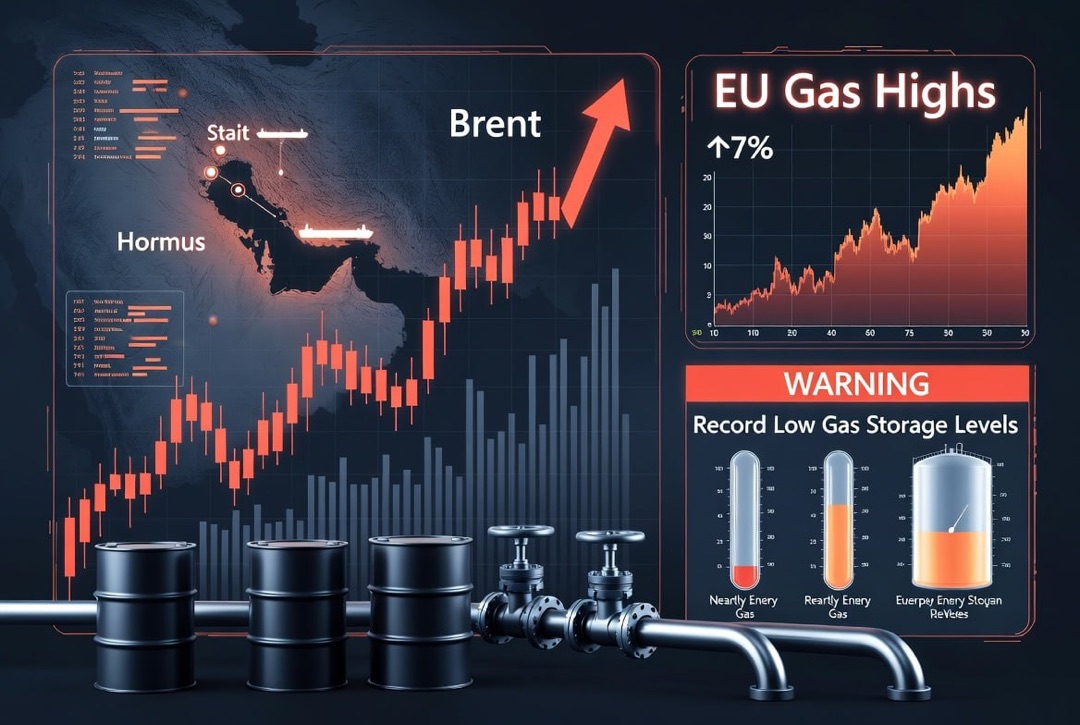

The main news for the oil market is a sharp decline in prices following reports of possible diplomatic progress surrounding the Strait of Hormuz. Brent fell to the mid-$90 per barrel range, while WTI dropped even more sharply, reflecting expectations of a partial recovery in marine logistics and a reduction in the risk of raw material shortages.

However, for the oil market, this does not yet signify a full pivot back to a stable balance. Prices remain significantly above levels typical of a normal surplus market. A geopolitical premium persists in the quotes, as market participants have yet to receive definitive confirmation of a sustainable agreement and swift restoration of all supply routes.

Key factors for oil on May 28 include:

- Expectations regarding a potential opening of the Strait of Hormuz for commercial shipping;

- Continued supply disruptions of Middle Eastern oil;

- A decline in global inventories of raw materials and oil products;

- High market sensitivity to statements from the U.S., Iran, and Gulf countries;

- The approaching summer season demand for gasoline, diesel, and jet fuel.

For oil companies, the current situation creates an ambiguous background: high prices support cash flow in the upstream segment, but sharp volatility complicates hedging, logistics, refinery throughput planning, and long-term investment decisions.

OPEC+ and Supply Balance: The Market Awaits Signals on July Production

OPEC+ remains a central factor for the global oil market. Amid geopolitical restrictions and supply disruptions, the alliance needs to balance two tasks: avoiding supply shortages while also preventing a drastic fall in prices from a sudden increase in production.

Investors are closely monitoring preparations for the June discussion on production parameters for July. Even a moderate increase in quotas may be interpreted by the market as a signal from producers to stabilize supply. However, the actual ability to ramp up exports depends not only on OPEC+ decisions but also on the safety of maritime routes, tanker fleet availability, cargo insurance, and regional infrastructure conditions.

For the energy market, this means that formal quotas are becoming less effective as standalone benchmarks. The real physical availability of oil, the speed of logistical restoration, and the ability of buyers to redistribute purchases among the Middle East, Atlantic basin, the USA, Latin America, and other export destinations are becoming increasingly important.

Inventories and Oil Products: Refineries Operate Within a Tight Buffer

The situation with oil and oil product inventories remains tense. Strong withdrawals from both commercial and strategic reserves in the U.S. demonstrate that the market is already utilizing buffer mechanisms to compensate for disruptions in global crude trading.

This is particularly important for refineries. High processing throughput supports the production of gasoline, diesel, jet fuel, and other oil products, but limited raw material inventories increase the risk of margin fluctuations. If oil continues to decline in price faster than oil products, refinery margins may temporarily improve. However, if logistics deteriorate again, processors will face rising raw material costs, supply disruptions, and increased competition for high-quality grades of oil.

In the oil products market, investors should monitor three indicators:

- The dynamics of gasoline inventories ahead of the summer driving season;

- The levels of diesel and middle distillate stocks;

- Throughput rates of refineries in the U.S., Europe, India, China, and Middle Eastern countries.

For fuel companies and oil product traders, the primary risk lies not just in the price of oil but also in the potential divergence of regional balances. Some markets may face a shortage of diesel or jet fuel, while others may experience a temporary surplus due to reduced exports or changes in supply routes.

Gas and LNG: Europe and Asia Compete for Flexible Supplies

The gas market reacts to the same geopolitical signals as oil, but with its own logic. European gas prices have decreased amid hopes for a restoration of shipping through the Strait of Hormuz; however, the LNG market remains nervous. Any disruption in supply from the Middle East instantly intensifies the competition between Europe and Asia for available shipments of liquefied natural gas.

Europe continues to inject gas into storage ahead of the winter season, but inventory levels remain a critical risk factor. If Asia begins to attract LNG supplies more aggressively due to heat and rising electricity demand, European consumers may have to pay a higher premium for deliveries.

Against this backdrop, the strategic role of long-term contracts is strengthening. Deals for LNG supplies from North America, including projects in Canada and the U.S., are becoming part of a new architecture of energy security. For buyers, this provides an option to reduce dependence on unstable supply routes, while for producers, it offers a pathway to secure demand for decades to come.

Electricity: Heat, Data Centers, and Network Limitations

The electricity sector is emerging as one of the primary growth areas for demand in the global energy sector. In Europe and Asia, heat waves are driving up electricity consumption for air conditioning, while weak wind generation during certain periods increases load on gas and coal plants.

In Germany, rising daytime electricity prices underscored how sensitive the market has become to the combination of heat and reduced wind output. In Asia, network loads are also rising: India, Vietnam, China, Japan, South Korea, and Southeast Asian countries are facing increased cooling demand.

A separate structural factor is data centers and artificial intelligence. They are transforming electricity into a strategic resource for the digital economy. For energy companies, this opens opportunities in generation, networks, energy storage, and long-term supply agreements, but it simultaneously raises the reliability requirements of the energy system.

Renewable Energy Sources: Growth Continues, but Backup Generation Remains Critical

Renewable energy sources continue to strengthen their position in the global electricity market. Solar and wind generation are increasingly becoming a low-cost and rapid way to increase capacity, especially in regions with high fuel imports. For investors, renewable energy remains a long-term growth avenue, particularly when paired with network infrastructure, industrial batteries, and demand management systems.

However, the current energy crisis also highlights the flip side of the energy transition. The higher the share of solar and wind power, the more important flexible resources become: gas plants, hydropower, storage, inter-system flows, and managed demand. Without backup generation, the energy system becomes vulnerable during heatwaves, calm periods, or sudden surges in consumption.

Therefore, the key investment takeaway for the energy market is not to pit renewable energy against traditional generation, but to seek balance. The greatest resilience is obtained by countries and companies that simultaneously develop clean energy, networks, storage, and access to reliable fuels.

Coal: Asia Returns Demand Amid Heat and Expensive Gas

The coal market is once again receiving support from Asia. High temperatures, rising electricity consumption, and expensive LNG are driving energy companies to utilize coal generation more actively. China, India, Japan, South Korea, and Southeast Asian countries remain critical demand centers for energy coal.

For coal companies, this creates a favorable pricing environment, despite long-term pressures from climate policies. In the short term, coal remains an important resource for the reliability of energy systems, especially in areas where gas infrastructure is limited, and renewables cannot cover evening peak consumption.

Investors should consider that coal in 2026 remains not only as "old" fuel but also as a tool for energy security. At the same time, regulatory risks, emissions costs, financing restrictions, and ESG pressures persist.

What Matters for Investors and Energy Companies on May 28

For the global audience of investors and market participants in the energy sector, Thursday, May 28, 2026, appears to be a day of risk reassessment, rather than one of risk removal. Oil may decrease on hopes for the Strait of Hormuz, but the physical market remains tense. Gas and LNG are dependent on the competition between Europe and Asia. The electricity sector is under pressure from heat, data centers, and network constraints. Renewables are growing, but require backup resources. Coal maintains its importance as an insurance resource.

Key benchmarks for the day include:

- Confirmation or refutation of diplomatic progress regarding the Strait of Hormuz;

- Actual dynamics of tanker flows and marine cargo insurance;

- Oil, gasoline, and diesel inventories in the U.S.;

- Gas prices in Europe and Asia;

- Load on energy systems in Asia and Europe due to heat;

- Demand for coal generation and LNG supplies;

- Signals from OPEC+ regarding summer production.

The main conclusion for the market is that the global energy sector remains in a phase of heightened uncertainty, where short-term declines in oil prices do not negate the structural deficit of reliability. For oil companies, refineries, gas traders, electricity producers, renewable energy investors, and the coal sector, it is not only about prices but also about access to infrastructure, logistics, backup power sources, and long-term contracts.